In 2015, 195 countries signed the global climate deal at the Paris climate conference (COP 21). The Paris Agreement aims to set an action plan pursuing efforts to limit the temperature increase to 1.5°C. Each signatory shall submit a Nationally Determined Contribution (NDC), an estimation which embodies her goal in emission reduction. Last December in Madrid, Spain (COP 25), signatories came together to negotiate the Article 6 of the rulebook of the Paris Agreement, the implementation guideline entailing how governments can achieve their NDCs through voluntary international cooperation by using the market mechanism. In particular, a well-designed carbon market would allow the businesses to pitch in climate mitigation, and increase ambition through technology innovation and cost savings re-investment.

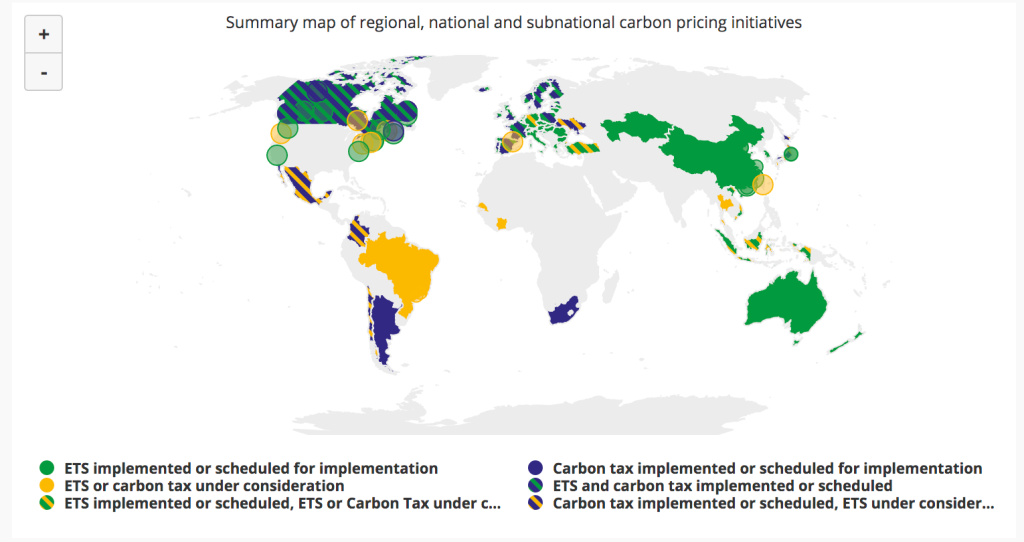

A carbon market is partly based on cap-and-trade programs. A jurisdiction puts a cap on allowable emissions on a scope of emission sources. Governments issue pollute permits and allow tradings between companies for permits. The goal is to achieve cost-effective emission reduction across the jurisdiction. As of 2019, there were 28 emissions trading systems (ETS) around the world at regional, national, and subnational levels (World Bank, 2019). New initiatives and regional ETS have started to launch and corporate. For example, the European Union and Switzerland linked their ETSs and entered into force this January. It is the first international linking emissions trading scheme covering around 2.7 billion tonnes of CO2 equivalent.

Parties see the benefits of participating in the global carbon market to boost economic development and achieve NDCs cost-effectively. However, there were discrepancies around the corresponding adjustment in Article 6.2 and baselines and additionality provisions in Article 6.4. The stalemate on Article 6.2 was to develop robust accounting for carbon markets. Double counting of credits occurs when a seller trades an emission reduction unit to a buyer and both claim emission cuts; as a result, only one unit of emission reduction is generated, but reported twice. This pattern poses a threat to achieve the emission reduction goal. It also makes mitigation progress less comparable and hard to track. In fact, it is estimated that 6.5% to 29.5% of global emissions are at the risk of being double-counted.

In COP 25, Brazil continued to oppose the corresponding adjustment in Article 6.2. Without that adjustment, loopholes in Article 6.2. could allow countries to achieve their carbon reduction goals without real emission reduction efforts. Brazil claimed that developing countries should be granted a period allowing double counting and promise to make up the emission debt later in 2030. The country made a commitment to reduce 37% CO2 emission by 2025 compared to her 2005 level, in fact, had reached the target in 2012, a 41% reduction compared to 2005 level. Double counting would allow Brazil to emit more while keeping good emission reduction records.

Another issue concerns the baseline and additionality in Article 6.4. The concept stems from the Clean Development Mechanism (CDM) under the Kyoto Protocol. It specifies the certified emission reduction credits that should only be given to the activities which would not happen under the counterfactual of the business-as-usual scenario. In the current situation where many NDCs are not ambitious enough to be far below business-as-usual, using carbon credits could generate “hot air” because of cheap carbon credits that do not represent real emission reductions. Further, renewable energy prices have decreased significantly and can compete with the cost of fossil-fueled energy. Pursuing a transition to renewable energy may become the business-as-usual and not a credit-rewarding activity that should be counted into NDCs. Thus, the additionality test plays a crucial role in the global market to prevent the ambition of NDCs to be attenuated. However, parties failed to agree on the definition, methodologies, and procedures for the additionality tests.

Though the issues of double counting and additionality persist, they do not prevent the development of regional trading schemes. We can learn from rules in regional systems and adjust to international implementable regulations. Little action is better than no action. The severity of climate change cannot wait for the protraction of international agreements.

Yu-Ting Lo

yutlo@umich.edu

References:

“World Bank Group. 2019. State and Trends of Carbon Pricing 2019. Washington, DC: World Bank. © World Bank. https://openknowledge.worldbank.org/handle/10986/31755 License: CC BY 3.0 IGO.”